by

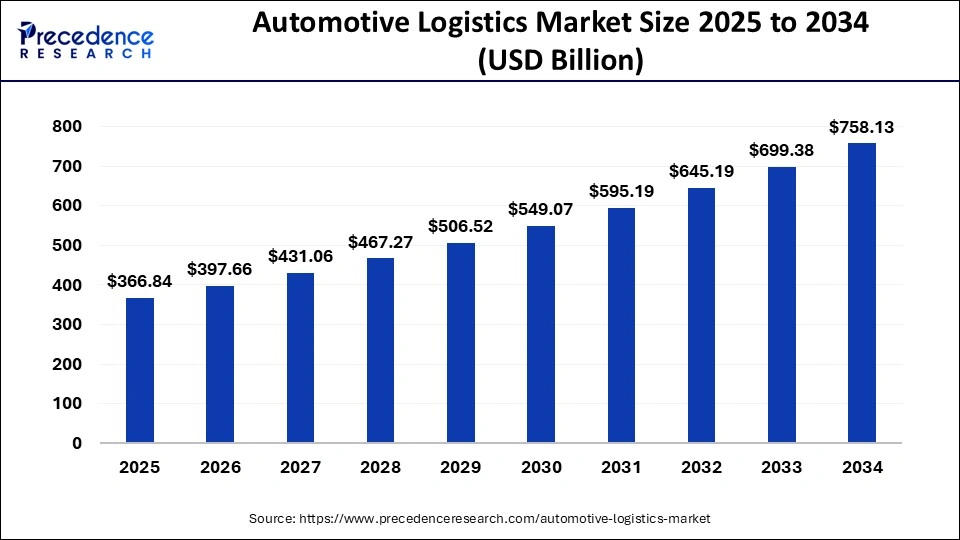

by The global automotive logistics market size accounted for USD 338.42 billion in 2024 and is predicted to cross USD 758.13 billion by 2034, at a CAGR of 8.4%.

Get Sample Copy of Report@ https://www.precedenceresearch.com/sample/1105

Key Insights

- With a revenue contribution exceeding 47%, Asia Pacific dominated the market in 2024.

- The automobile parts segment secured the largest market share by type in 2024.

- The finished vehicles segment is set to grow at a notable CAGR from 2025 to 2034.

- By activity, the transportation segment led the market with the highest revenue in 2024.

- The warehousing segment is expected to expand at the most rapid CAGR in the coming years.

Drivers

The growing demand for automobiles, coupled with increasing globalization, is a major driver for the automotive logistics market. As vehicle production expands across different regions, the need for efficient transportation, warehousing, and supply chain management has intensified.

The rise in electric vehicle (EV) production further drives the demand for specialized logistics solutions, particularly for handling lithium-ion batteries and other components. Additionally, advancements in digital logistics, such as real-time tracking, automation, and artificial intelligence, are improving operational efficiency and reducing transportation costs.

Opportunities

The integration of smart logistics and IoT-based tracking systems presents significant opportunities in the automotive logistics market. Companies are investing in real-time tracking, predictive analytics, and autonomous logistics solutions to enhance supply chain transparency and efficiency.

The expansion of e-commerce in the automotive sector has also increased demand for faster and more reliable logistics solutions. Additionally, emerging markets in Asia-Pacific and Latin America offer growth potential, as governments invest in infrastructure development and manufacturing facilities expand in these regions.

Challenges

One of the major challenges in the automotive logistics market is supply chain disruptions caused by geopolitical tensions, raw material shortages, and fluctuating fuel prices. The complexity of managing global supply chains, especially in an industry heavily reliant on just-in-time (JIT) manufacturing, adds to the difficulties.

Additionally, environmental concerns and stringent emission regulations are pushing logistics companies to adopt greener transportation methods, which require substantial investment. The rising cost of warehousing and labor shortages further impact market growth.

Regional Analysis

Asia-Pacific holds the largest share in the automotive logistics market due to its strong manufacturing base in countries like China, India, and Japan. North America follows closely, driven by a high demand for EVs and the presence of major automakers. Europe is also a key market, with strong logistics infrastructure supporting automotive supply chains.

Meanwhile, Latin America and the Middle East & Africa are emerging as potential markets, supported by increasing automobile production and improving transportation networks.

Automotive Logistics Market Companies

- CEVA Logistics

- BLG LOGISTICS GROUP AG & Co. KG

- Hellmann Worldwide Logistics

- Ryder System, Inc.

- GEFCO

- CFR Rinkens

- Penske Automotive Group, Inc.

- Imperial Logistics

- Expeditors International of Washington, Inc.

- Nippon Express Co. Ltd.

- Kerry Logistics Network

- Schnellecke group ag& co. Kg

Companies Share Insights

The global automotive logistics market is oligopolistic in nature and dominated by the some of the key players operating in the market. Market players are incorporating advanced technologies for route optimization, real-time tracking of shipments, and also provide technology-driven services to their customers. Collaboration, merger & acquisition of various other automotive logistics companies are the prime strategies adopted by the industry participants to capture maximum revenue share in the market. Furthermore, the market players are also focusing to improve their automation technology to achieve a competitive advantage among different end-users.

Segments Covered in the Report

By Type

- Automobile Parts

- Finished Vehicle

By Activity

- Transportation

- Airways

- Roadways

- Railways

- Maritime

- Warehousing

By Logistics Solution

- Outbound

- Inbound

- Reverse Distribution (International and Domestic)

By Distribution

- International

- Domestic

By Regional Outlook

- North America

- U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Asia Pacific

- China

- India

- Japan

- South Korea

- Rest of the World

Ready for more? Dive into the full experience on our website@ https://www.precedenceresearch.com/