by

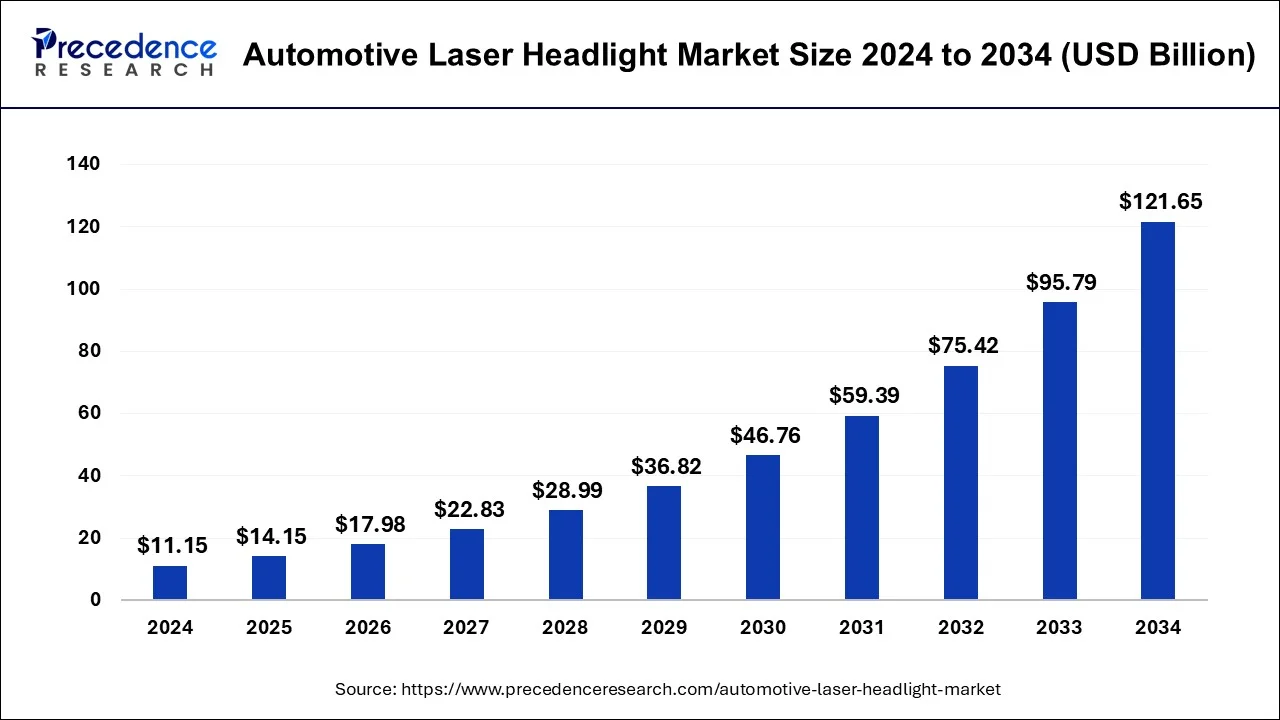

by The automotive laser headlight market size is expected to attain around USD 121.65 billion by 2034 increasing from USD 11.15 in 2024, growing at a CAGR of 26.8%.

Get Sample Copy of Report@ https://www.precedenceresearch.com/sample/1049

Key Takeaways

- Europe led the global market with the highest market share of 40% in 2023.

- By Vehicle Type, the Passenger vehicle segment has held the largest market share in 2023.

- By Technology, the intelligent laser headlight segment had the largest market share in 2023.

Market Drivers

Advancements in automotive lighting technology and increasing demand for high-performance headlights are key factors driving the automotive laser headlight market. Laser headlights offer superior illumination, allowing drivers to see further distances with enhanced clarity. The growing adoption of luxury and high-end vehicles, where advanced lighting systems are a standard feature, is also fueling market growth. Additionally, environmental concerns and the push for energy-efficient vehicle components are encouraging automakers to integrate laser headlights into their designs.

Opportunities

The ongoing innovation in adaptive and intelligent lighting systems provides significant growth opportunities for the market. The shift toward electric vehicles and smart cars is further driving the demand for efficient and advanced lighting solutions. Collaborations between automotive manufacturers and technology firms to develop cost-effective laser headlight systems can help expand their adoption. Emerging markets with increasing vehicle production and improving infrastructure are also expected to boost market penetration in the coming years.

Challenges

The market faces challenges related to the high cost of laser headlights, which limits their use in mass-market vehicles. Technical hurdles, such as the complexity of production and potential overheating issues, pose additional difficulties. Strict regulatory guidelines concerning laser intensity and driver safety create barriers for widespread adoption. Furthermore, the presence of alternative lighting technologies, such as matrix LED and OLED headlights, adds competitive pressure to the market.

Regional Analysis

Europe and North America continue to lead the market due to strong research and development efforts and high adoption rates of luxury vehicles. The Asia-Pacific region is rapidly expanding, fueled by increasing consumer demand for advanced vehicle technologies and government initiatives supporting automotive innovation. China, Japan, and South Korea are emerging as major contributors to market growth. Meanwhile, regions like the Middle East and Africa are gradually adopting laser headlight technology, with rising investment in the automotive sector creating new opportunities for manufacturers.

Automotive Laser Headlight Market Companies

- OSRAM GmbH

- SLD Laser

- Valeo SA

- ZKW Group

- LASER Component

- Koito manufacturing Co. Ltd

- Palomar Technologies

- Hella GmbH & Co. KGaA

- Marelli Holdings Co. Ltd.

- Koninklijke Philips N.V.

Key Companies Share Insights

The global automotive laser headlight market is dominated with the presence of leading automotive light manufacturers such as OSRAM GmbH, Valeo S.A., Hella GmbH & Co. KGaA, SLD Laser, and others. These market players are exclusively focused towards expanding their footprint in the global market through merger & acquisition and product development. For instance, in December 2019, SLD Laser launched LiFi Communication and sensing technologies for consumer and automotive applications. Similarly, in 2018, OSRAM GmbH introduced laser-based light sources or application specific LEDs in wide range of designs, mainly for automotive forward lighting and general lighting applications. The company also developed infrared lasers and high-efficiency visible for sensor and projection applications such as Adaptive Cruise Control (ACC) system in vehicles.

Segments Covered in the Report

By Technology

- Intelligent

- Conventional

By Vehicle Type

- Commercial Vehicle

- Passenger Vehicle

By Sales Channel

- Aftermarket

- OEM

By Regional Outlook

- North America

- U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Asia Pacific

- China

- India

- Japan

- South Korea

- Rest of the World

Ready for more? Dive into the full experience on our website@ https://www.precedenceresearch.com/